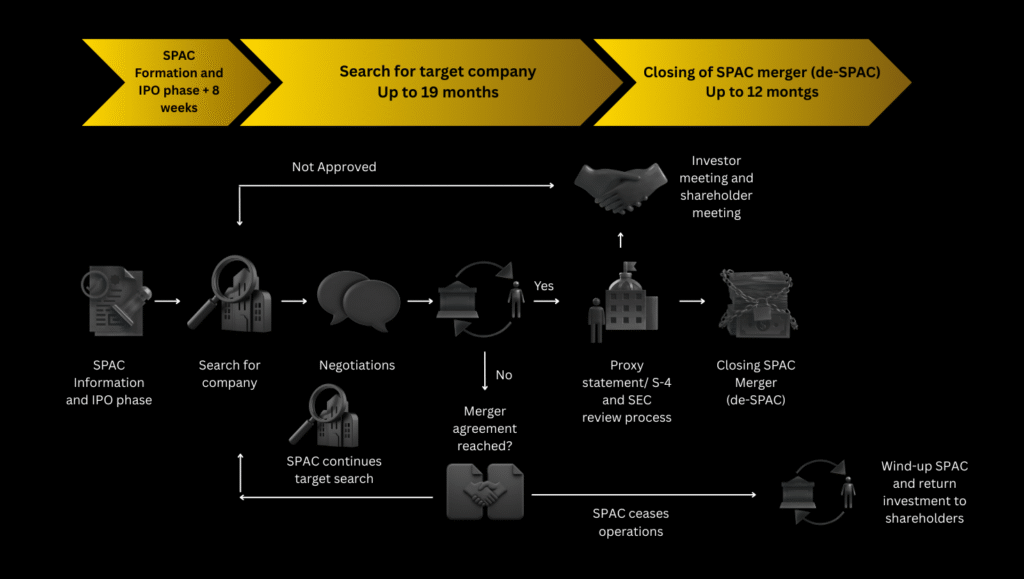

What is a SPAC?

Special purpose acquisition companies (SPACs) have become a preferred

way for many experienced management teams and sponsors to take

companies public. A SPAC raises capital through an initial public offering

(IPO) for the purpose of acquiring an existing operating company.

Subsequently, an operating company can merge with (or be acquired by)

the publicly traded SPAC and become a listed company in lieu of executing

its own IPO.

This approach offers several distinct advantages over a traditional IPO,

such as providing companies access to capital, even when market volatility

and other conditions limit liquidity. SPACs could also potentially lower

transaction fees as well as expedite the timeline to become a public

company.

However, the merger of a SPAC with a target company presents several

challenges, including having to meet an accelerated public company

readiness timeline as well as complex accounting and financial

reporting/registration requirements that may differ based upon the lifecycle

of the SPAC involved. The target company's management team will need

to focus on being ready to operate as a public company within three to five

months of signing a letter of intent.